New Industry Report Forecasts Generative AI Enterprise Adoption and Market Growth Through 2034

The Trillion-Dollar Bet: Mapping the Future of Generative AI Through 2034

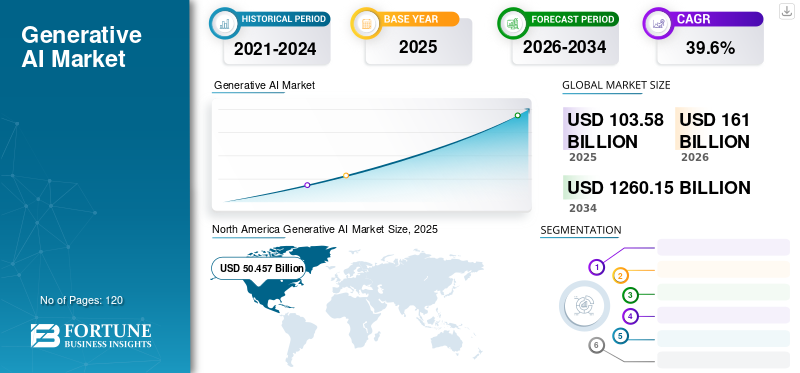

The global generative AI market is currently sprinting through a growth phase that borders on the frantic. Recent industry projections suggest the sector is ballooning from a valuation of roughly $103.58 billion in 2025 to a staggering $1.26 trillion by 2034. We’re looking at a compound annual growth rate (CAGR) of 29.30%, a figure driven by a simple reality: enterprises have stopped treating AI as a shiny new toy and started treating it as the engine room of their operations. From manufacturing floors to IT departments and energy grids, the mandate is clear—automate, integrate, or fall behind.

From Experimentation to Infrastructure

Not long ago, generative AI was the domain of researchers and Silicon Valley hobbyists. Today, it’s the backbone of enterprise strategy. The shift has been seismic, moving from basic text-generation prompts to the deployment of complex foundation models: multimodal LLMs, diffusion models, and generative adversarial networks (GANs).

Companies aren't just playing with these tools anymore; they are embedding them into their workflows to handle the heavy lifting—data processing, predictive maintenance, and complex task automation that once required armies of human analysts. But reaching that trillion-dollar milestone won't be a smooth ride. The ecosystem is currently wrestling with a cocktail of regulatory friction, rising operational costs, and the cold reality of new U.S. tariff policies that threaten to complicate the hardware supply chain.

The Geographic and Competitive Power Centers

If you want to know where the AI revolution is headquartered, look at North America. As of 2025, the region commands 48.70% of the market. This isn't an accident; it’s the result of massive, sustained capital expenditure in computational infrastructure and a concentration of the world’s most influential developers. However, keep a close eye on the Asia Pacific region. It is currently the fastest-growing market, suggesting that the center of gravity for AI adoption is beginning to tilt eastward.

The market’s current structure is, frankly, a bit of an oligarchy. According to data from Global Market Insights Inc., the top five players—OpenAI, Anthropic, NVIDIA, Adobe, and Microsoft—controlled over 58% of the market in 2025. OpenAI alone held nearly a quarter of the pie, a testament to the "first-mover" advantage that defined the early era of foundation models.

The current competitive hierarchy looks like this:

- OpenAI: The undisputed heavyweight in model development.

- Microsoft: The primary architect of enterprise integration and cloud-based deployment.

- Google: Leveraging massive scale to weave AI into search and enterprise ecosystems.

- NVIDIA: The indispensable hardware kingpin; without their chips, the lights go out.

- Adobe: Dominating the creative and generative media space.

- Enterprise Specialists: Players like SAP, IBM, AWS, Rephrase AI, and Synthesis AI are carving out critical niches in sectoral applications.

The Cost of Innovation

While the generative AI market is undeniably bullish, the industry is feeling the pinch. Training large-scale models is expensive, and keeping the data centers running is even more so. Firms are now caught in a balancing act: how do you innovate at breakneck speed while maintaining cost-efficiency? This is further complicated by trade barriers and tariffs on specialized AI hardware, which are forcing companies to rethink their supply chains.

| Metric | 2025 Data | 2034/2035 Projection |

|---|---|---|

| Market Valuation | USD 103.58 Billion | USD 1,260.15 Billion |

| Primary Leader (2025) | OpenAI (23.6% share) | N/A |

| Top 5 Concentration | 58.1% (2025) | N/A |

| Projected CAGR | N/A | 29.30% (to 2034) |

The Multimodal Shift

The real game-changer isn't just "smarter" text—it’s the move toward multimodal systems. By processing text, audio, video, and imagery simultaneously, these models are becoming genuinely useful in physical industries. In manufacturing, they’re predicting equipment failures before they happen. In IT, they’re drafting system architectures.

As hardware becomes more efficient, we’re seeing a push toward "edge AI"—running these complex models closer to the data source. This reduces latency, improves real-time performance, and ultimately makes AI a more practical tool for the average enterprise.

Navigating the New Ecosystem

The generative AI market report makes it clear: the ecosystem is in the middle of a structural overhaul. Beyond the economics, there is a mounting pressure regarding regulatory compliance and ethical deployment. Companies are no longer just asking, "Can we build it?" They’re asking, "Is it transparent? Is it private? Is it sustainable?"

This scrutiny is driving a shift toward hybrid cloud models and decentralized deployment. The goal is to mitigate the risks of relying on a single, centralized provider. As the market matures, the conversation is shifting from "What can this model do?" to "What is the measurable ROI?"

The Road to 2035

The long-term outlook remains strong, even if the path ahead is littered with regulatory and economic speed bumps. Reaching a trillion-dollar valuation by 2035 isn't a guarantee; it’s a target that assumes the industry can successfully navigate its own growing pains.

The next decade will likely be defined by four key factors:

- Hyper-Competition: Expect new entrants to challenge the current leaders, leading to a surge in specialized, domain-specific AI tools.

- Regulatory Maturity: Companies that successfully align with international AI governance standards will be the ones that survive the coming shakeout.

- Hardware Hunger: The demand for high-performance computing (HPC) and specialized chips will remain the primary engine of capital expenditure.

- Verticalization: The "one-size-fits-all" model is fading. The future belongs to models trained on specific, proprietary industry data.

We are currently in the "scaling" phase of the generative AI era. The novelty of the early days has worn off, replaced by the hard work of integrating these systems into the foundational layers of the global economy. The transition from novelty to necessity is nearly complete. Whether the industry can manage the rising operational costs and geopolitical trade tensions will determine the final shape of this new digital landscape. One thing is certain: the era of data-driven, automated decision-making is no longer on the horizon—it is already here.